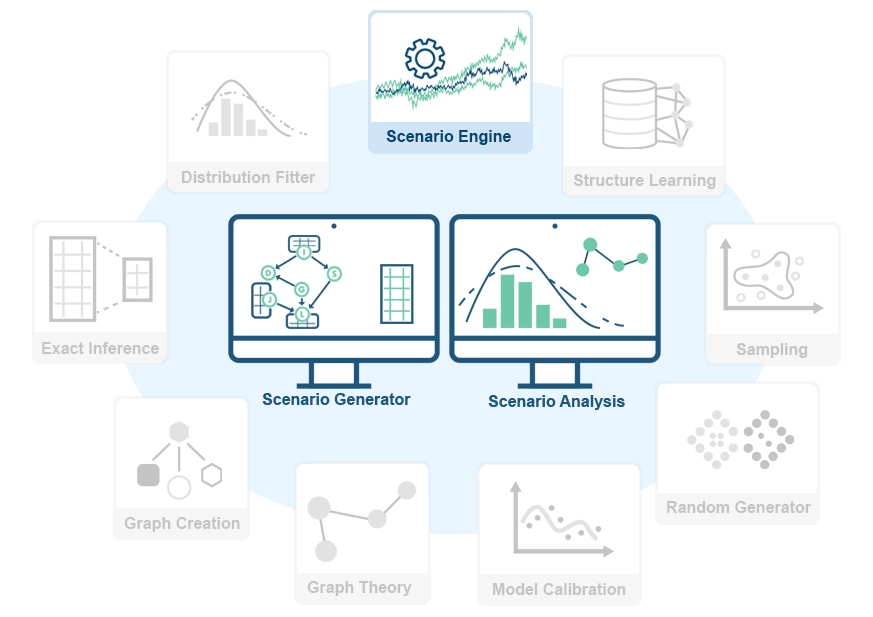

TKRISK Scenario Engine Module

✔ Multi-factor Scenario Generation

Create scenarios incorporating multiple risk factors and their interdependencies, capturing the complexity of real-world situations.

✔ Stochastic Path Simulation

Generate realistic time-evolving scenarios using advanced stochastic processes and time series models.

✔ Scenario Library

Access a comprehensive library of pre-defined scenarios based on historical events, regulatory requirements, and expert knowledge.

✔ Customizable Scenario Templates

Create and save custom scenario templates tailored to your specific risk management needs and industry requirements.

- Extreme Value Scenario Generation: Model tail risk events and rare scenarios using advanced extreme value theory techniques.

- Conditional Scenario Generation: Create scenarios conditioned on specific events or outcomes to explore targeted risk situations.

- Reverse Stress Testing: Identify scenarios that could lead to specific adverse outcomes, helping to uncover hidden vulnerabilities.

- Scenario Blending: Combine multiple scenarios to create complex, multi-faceted risk narratives.

- AI-Driven Scenario Generation: Leverage machine learning algorithms to generate novel and plausible scenarios based on historical data and expert input.

- Utilize probabilistic models from the Graph Creation module to inform scenario generation.

- Incorporate fitted distributions from the Distribution Fitter module for realistic scenario parameters.

- Feed generated scenarios into the Sampling module for comprehensive Monte Carlo simulations.

- Use the Inference module to analyze the likelihood and impact of generated scenarios.

- Finance: Generate market scenarios for stress testing, portfolio optimization, and regulatory compliance (e.g., CCAR, ICAAP).

- Insurance: Model catastrophe scenarios, simulate claims environments, and assess long-term policy risks.

- Energy: Create scenarios for energy price fluctuations, demand changes, and regulatory shifts.

- Supply Chain: Simulate disruption scenarios, demand shocks, and geopolitical events affecting global supply networks.

- Climate Risk: Generate climate change scenarios to assess long-term environmental and economic impacts.

- Supports generation of millions of complex, multi-factor scenarios.

- Implements efficient algorithms for fast scenario generation, even for high-dimensional models.

- Provides parallel processing capabilities for improved performance on multi-core systems and distributed environments.

- Offers a comprehensive API for seamless integration with external data sources and custom scenario generation workflows.

- Includes advanced visualization tools for scenario analysis and comparison.

Get Started with Advanced Scenario Engine

Enhance your risk management strategies with TKRISK's powerful Scenario Engine module.

Whether you're stress testing financial portfolios, assessing insurance risks, or planning for climate change impacts, our advanced scenario generation capabilities provide the comprehensive insights you need for robust decision-making in uncertain environments.